The Strategy: In 2026, with inflation running around 2.4%, the math behind low-interest debt has shifted. A 3%–4% mortgage is no longer just a loan—it is a mathematical hedge. Understanding the impact of inflation on mortgage debt is the key to deciding between extra payments and capturing the wealth spread in the market.

Inflation and the “Shrinking Dollar” Effect

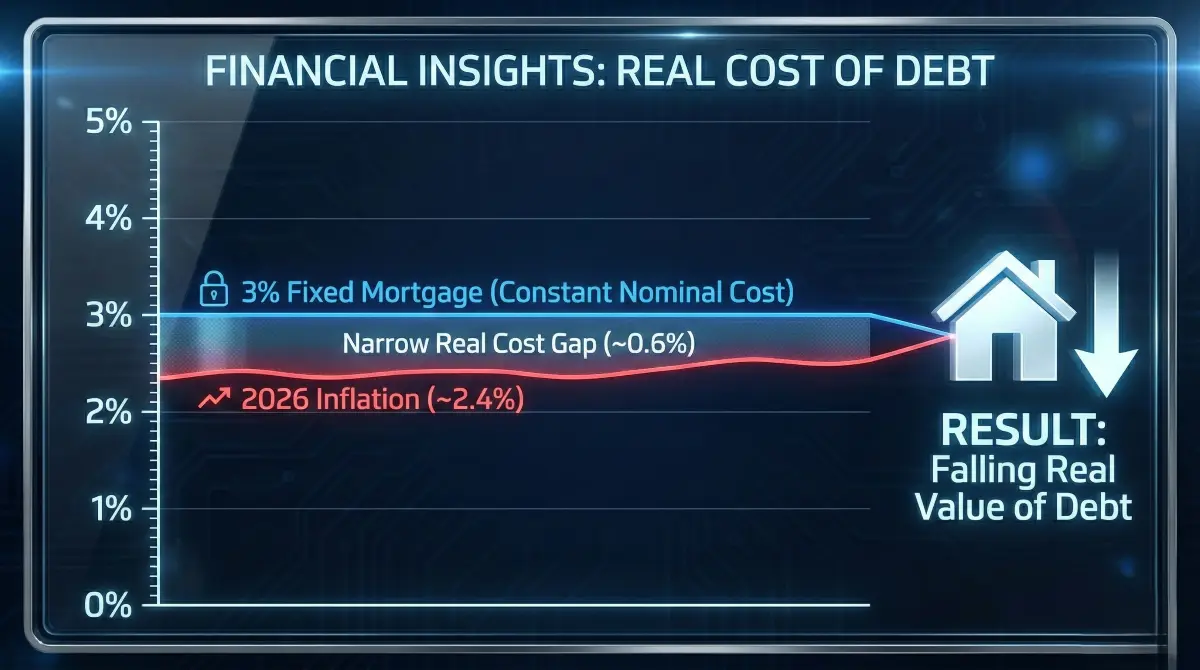

Inflation quietly changes how debt works. When prices rise, each future dollar you use to repay a loan has less purchasing power than the dollars you originally borrowed. This is the “shrinking ruler” effect: your debt stays fixed in nominal terms, but the economic “weight” of that debt decreases every year.

Think of it this way: if you owe someone 10 pizzas today, and by the time you pay them back, pizzas have shrunk to half their size, you’ve effectively kept half the value for yourself. In 2026, your fixed-rate debt is that shrinking pizza.

The Math: The Fisher Equation

Economists describe this relationship using the Fisher equation, which reveals your “real” interest rate (r). If your mortgage rate is 3.5% (i) and inflation is 2.4% (π), your real borrowing cost is only 1.1%:

This makes a 3% mortgage an incredible hedge, as you are repaying the bank with devalued currency while your home value likely tracks or exceeds inflation.

Tax Changes: The OBBBA Factor

The 2025 passage of the One Big Beautiful Bill Act (OBBBA) shifted the landscape. With adjusted income brackets and a higher standard deduction, your “after-tax cost of debt” is the metric that truly matters. For those who itemize, mortgage interest remains a primary tool to lower taxable income, making a 3–4% loan even cheaper in real terms.

If you can earn 10–12% in the equity markets while paying only 3% on a loan, the “spread” is wealth created for your future self. However, this requires a nuanced comparison against your specific tax bracket.

📊 Run Your 2026 Scenario

Don’t let emotion dictate your balance sheet. What is your real interest rate after inflation? Use our simulator to factor in the new OBBBA tax thresholds.

Test Your Scenario →When Acceleration Makes Sense

Inflation helps fixed-rate debt, but it cannot outrun high interest rates. With credit card APRs hovering between 23–25% in 2026, the math changes instantly. No investment strategy reliably beats a guaranteed 24% return.

- •Credit Cards: Always the #1 priority for repayment.

- •High-Rate Student Loans: If your rate is above 7%, accelerated payoff is often mathematically superior.

- •Low-Rate Mortgages: These are often your best long-term assets in a 2.4% inflation world.

Frequently Asked Questions

Is a 3% mortgage better than investing during inflation?

Yes. High inflation erodes the “real” value of your debt. If inflation is 3% and your mortgage is 3%, your real interest rate is 0%, making the debt effectively free.

How does the OBBBA change the math?

The higher standard deduction means fewer people benefit from the mortgage interest deduction, which can increase your effective after-tax rate. Our simulator accounts for these new tax brackets automatically.