Inflation is usually discussed as a burden—rising costs and shrinking margins. However, through a balance sheet lens, inflation is the silent partner of the fixed-rate borrower.

A mortgage or a student loan agreement is written in nominal dollars. If you borrowed $400,000, that is the immutable number printed on the contract. However, inflation affects real purchasing power. As the prices of goods and services rise over time, each future dollar used to repay the debt represents less economic value than it did on the day the contract was signed.

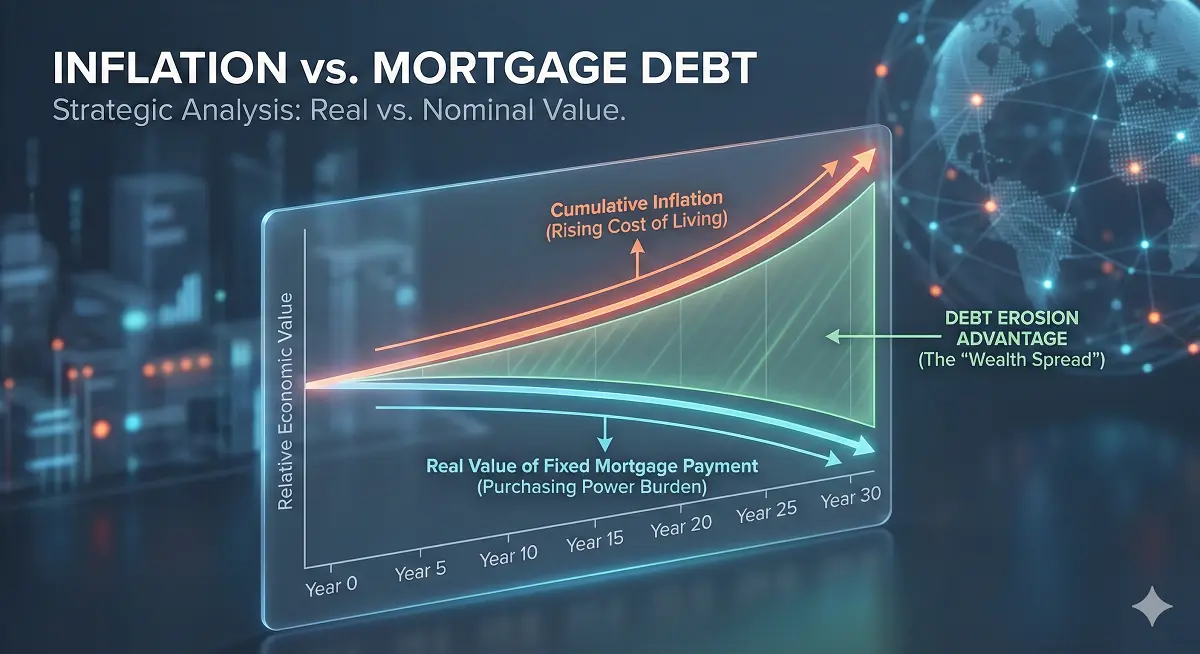

Economists describe this as the gap between nominal and real value. In a moderate inflation environment, the real burden of a fixed-rate loan gradually declines, even if you only make the minimum scheduled payments.

Fixed Payments in a Rising Environment

Consider a fixed monthly payment of $2,500. Today, it might represent a significant portion of your household income. If wages and prices rise over the next decade, that same $2,500 payment remains static, representing a smaller percentage of your total cash flow. The payment does not adjust upward, even though the broader economy does.

“A fixed-rate loan acts as a ‘short position’ on the currency. You are essentially capturing the spread between rising asset prices and static debt costs.”

Asset Values and Loan Structure

Historically, housing and broad market assets have tended to move in line with long-term inflation. When property values rise while a mortgage balance amortizes at a fixed rate, equity increases from two directions: property appreciation and the gradual reduction in the real value of the underlying debt.

The Math: The Fisher Equation

The relationship between your nominal interest rate and inflation is expressed via the Fisher Equation. This reveals your Real Interest Rate (r):

(Where i is the nominal interest rate, and π is the inflation rate)

With inflation at 2026 levels, a 4% mortgage might imply a real interest rate of approximately 1.5% before taxes. This calculation is the foundation of strategic capital allocation—helping you decide if your cash works harder in early repayment or in diversified investments.

Run your specific numbers:

Separating Psychology from Math

The desire to be debt-free is a valid psychological goal. For many, the emotional relief of owning an asset outright exceeds the mathematical “spread” found in a spreadsheet. Financial decisions are rarely purely logical; they are human.

However, our mission is to ensure that if you choose to accelerate your payoff, you do so with full data sovereignty. Understanding that your debt is being eroded by inflation allows you to weigh the “peace of mind” against the potential long-term opportunity cost of capital.