The Strategy: If your mortgage rate is sitting at 6% or 7%, the old advice of “just invest the difference” starts to break down. When debt was cheap (3%), the math was easy. Now, it’s a battle of the spreads. As an analyst, I prefer looking at the Real Spread rather than following emotional “debt-free” hype or bank-led investment pushes.

The Guaranteed vs. Speculative Spread

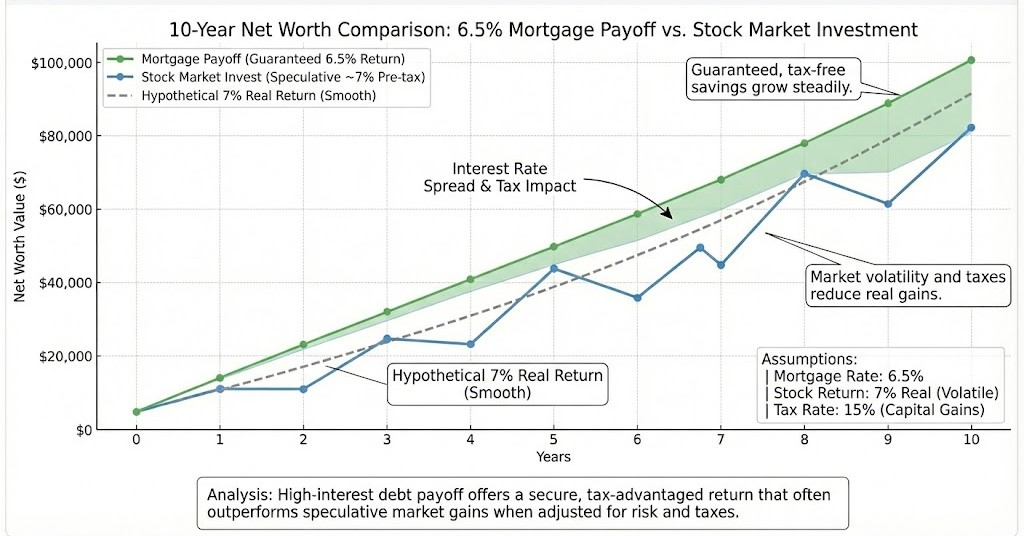

In purely mathematical terms, investing wins when expected stock returns (Rs) are higher than your mortgage rate (i). Historically, the S&P 500 returns roughly 7% after inflation. However, that return is speculative. Paying off a 6.5% mortgage is a guaranteed return of exactly 6.5%.

Analytic Note on “Apples-to-Apples” Clarity: This compares real stock returns (~7%) to your nominal mortgage rate (6.5%). While nominal stock returns are higher (~10%), once you subtract inflation, capital gains taxes, and account for market volatility, the effective “win” for investing often disappears when debt interest exceeds 6%.

Graph Assumptions & Inputs:

- Mortgage Rate: 6.5% (Guaranteed)

- Stock Returns: 7% Real (Historical S&P 500 avg, simulated with volatility)

- Taxes: 15% Capital Gains Tax on investment growth

- Inflation: 3% constant (used for real return calculation)

The Hidden Math: Taxes and Inflation

Two factors change the result significantly: taxes and inflation. Paying off debt is a tax-free return. To match a 6.5% tax-free return in the market, you must earn a higher nominal return to account for what the IRS takes.

Regarding inflation, we must look at the Real Interest Rate (r). Even in 2026, if inflation (π) is lower than your nominal rate (i), your debt is still growing in real terms:

A high interest rate like 6.5% typically outpaces average inflation. This keeps the “real burden” of your debt heavy, making aggressive repayment a mathematically sound way to secure your balance sheet.

Explore Other Mathematical Scenarios:

- Low Rates: See why the math changes for a 3% Mortgage vs. Investing.

- Inflation Mechanics: Visualize how Inflation Lowers Your Real Debt Burden.

- Student Wealth: Compare the 6% Rule for Student Loans using our specialized simulator.

Frequently Asked Questions

Is a 7% mortgage too high to justify investing?

Mathematically, for most people, the answer is yes. To beat a 7% guaranteed return, you’d likely need a 9%+ nominal market return to break even after taxes. That’s a high bar for the stock market to hit consistently in any 10-year window.

Does volatility affect the decision?

Yes. A 7% mortgage payoff is “smooth”—your net worth increases predictably every month. Stock market returns are “lumpy.” If the market drops 20% while you are holding 7% debt, your net worth takes a double hit from interest costs and market loss.

The Bottom Line: High-interest debt (6%+) is an investment opportunity in disguise. You aren’t just “paying off a loan”—you are buying a guaranteed, tax-advantaged return. Use our Wealth Builder Simulator to see how this affects your 2026 projections.